Share on Social 👇

Treatment of Income Tax on Shares: Capital Gains or Business Income

{kind=link}

Income from transfer shares can be either treated under the head “Income from Business” or “Income from Capital Gains”.

People make Investments for the purpose of generating more sources of income. And, one such source of investment could be investing in shares or mutual funds. Further, investing your earnings in shares or mutual funds could be sahi hai as shown in the ads in newspapers and televisions, but it requires the due attention of the investor to the disclaimer that the shares are subject to market risk, read all the documents carefully before investing.

Let’s have a look at, how can you treat income from transfer of shares.

On the contrary to the above, if you do not do significant trade activity or trade-in Future of Options, then you can treat income from the transfer of shares as capital gains. Further, the capital gain is when the sale price is more than the purchase price.

In addition to the above, earnings from capital gains are dependent on three factors:

- Firstly, the period of holding of shares

- Secondly, the nature of the instrument – shares, equity mutual fund or debt mutual fund, and

- Thirdly, payment of STT (Securities Transaction Tax)

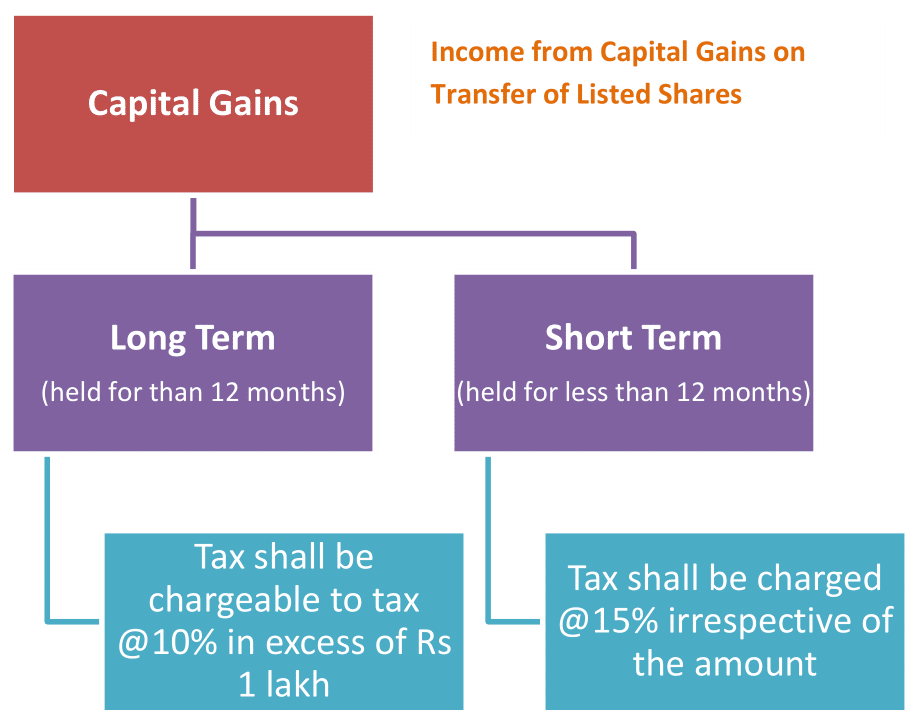

Capital Gains have been classified into two types:

- Long Term Capital Gains

- Short Term Capital Gains

- If the holding of listed shares is for more than 12 months, then the gains from the transfer of shares shall be classified as Long Term Capital Gains. Accordingly, tax shall be chargeable to tax @10% above Rs. 1 lac.

- On the other hand, if the holding of listed shares is for less than 12 months, then the gains from the transfer of such shares are Short Term Capital Gains. Accordingly, tax shall be chargeable @15% irrespective of the amount.

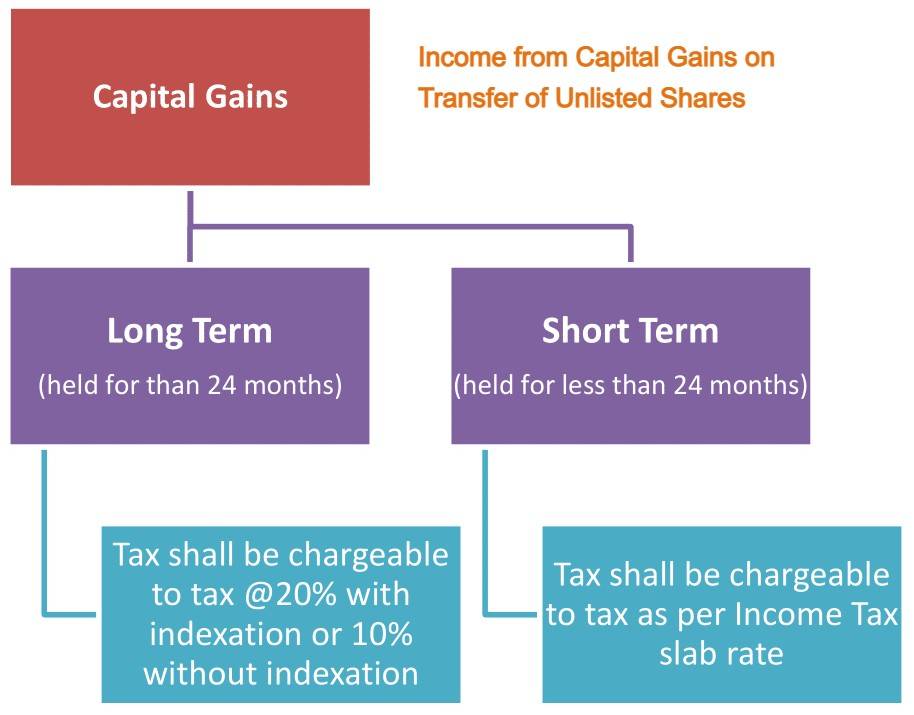

Unlisted Shares, the holding of which for more than 24 months are Long Term Capital Gains. Whereas, the shares whose holding period is less than 24 months are Short Term Capital Gains.

Note:

This is with effect from Assessment Year 2017-2018.