Income Tax On Income Of Minor Child – Treatment of Income of a Minor Child

View this post on Instagram

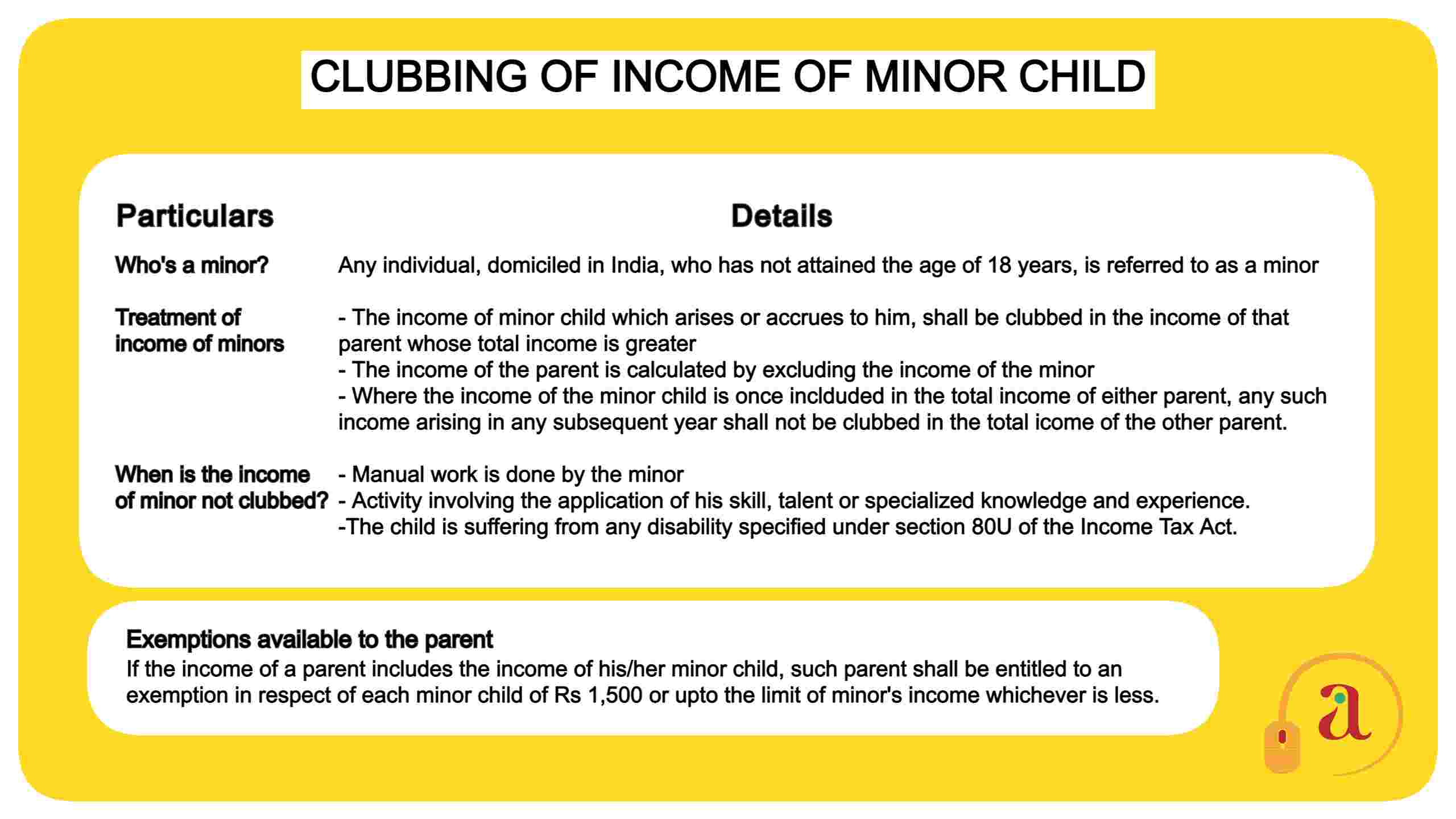

Many people think that the income earned by the minors is not taxable and if they transfer their income earned to their minor child, then it will lead to reduction of their tax liability. However, as per the provisions of Section 64 of Income Tax Act, if the minor earns any income, then that is clubbed with the income of their parents.

Clubbing of Income, in simple terms means that the income of one person is clubbed in the income of the other person. This clubbing of income can be done with the income of spouse, income of minor child, income from assets transferred to son’s wife/spouse, and so on. Having stated this, the income earned by minor is also taxable under the Income Tax Act.

The income of minor child which arises or accrues to him, shall be clubbed in the income of that parent (mother/father) whose total income is greater.

Note:

– The income of the parent is calculated by excluding the income of the minor child under Section 64(1A) of the Act.

– The child also includes step child and adopted child.

In a case where the income of the minor child is once included in the total income of either parent, any such income arising in any subsequent year shall not be clubbed in the total income of the other parent, unless the A.O. (Assessing Officer) is satisfied, after giving an opportunity of being heard to that parent, that it is necessary so to do.

Illustration:

Illustration: