TDS On Insurance Commission (Section 194D)

View this post on Instagram

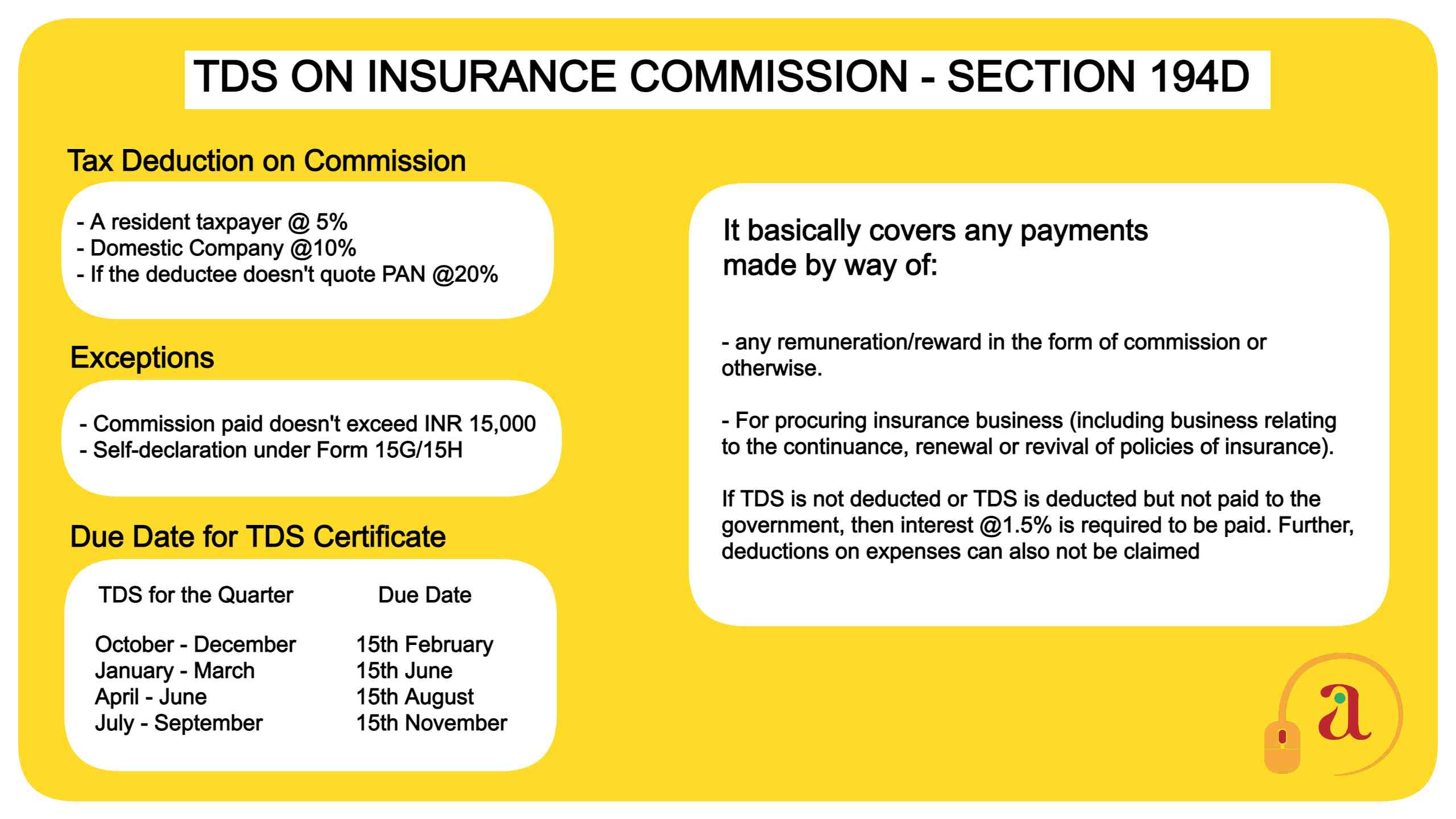

TDS under Section 194D is to be deducted in case any person who pays to resident an income in form of remuneration/reward for generating insurance business.

When you buy an insurance policy through an agent, he receives commission, remuneration or reward. Such commission, remuneration or reward attracts TDS under Section 194D of the Income Tax Act

👉Click Here to File You TDS Return👈