Share on Social 👇

The New Section 194S – All You Need To Know

Section 194S was introduced in the Income Tax Act, 1961 just like Section 194R through the Finance Act, 2022. Thereby, as per Section 194S, there shall be a deduction of TDS @1% on the transfer of Virtual Digital Assets (VDA). Further, the provisions of this Section shall come into effect from July 1, 2022.

The provisions of Section 194S apply to all persons i.e.,

- Individuals

- HUFs

- Partnership Firms (including LLPs)

- Companies

- Others

However, for the threshold limit for the calculation of TDS, the individuals and HUFs are classified as “specified persons”. Whereas, the rest of the persons are “other than specified persons”.

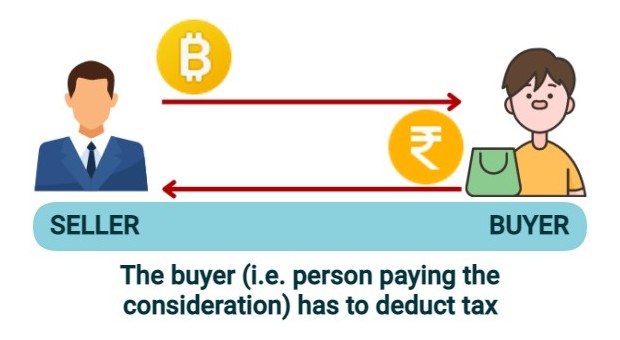

As per Section 194S of the Act, any person who is responsible for paying to any resident any sum by way of consideration for transfer of VDA has to deduct tax. Therefore, in a peer to peer (i.e. direct buyer to seller) transaction, the buyer (i.e., person paying the consideration) has to deduct tax.

If there is transfer of Virtual Digital Asset through exchange, then only the exchange can deduct the TDS under Section 194S. This is so because through the exchange.

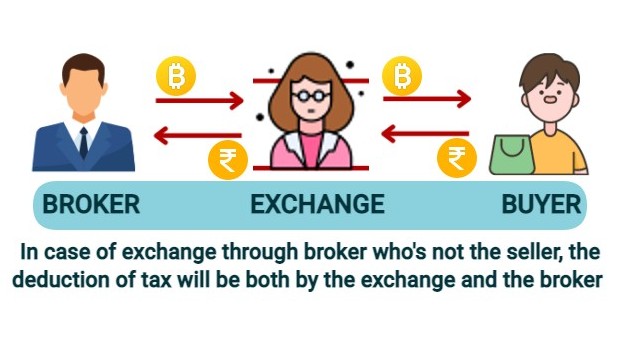

Transfer Of VDA On An Exchange Through A Broker Who Is Not The Seller

As per the circular on Section 194S by the Income Tax Department, in the case of exchange through a broker who is not the seller, the deduction of tax will be both by the exchange and the broker. However, if there is a written agreement between the exchange and the broker that only the broker will be deducting tax, then the broker may alone deduct the tax.

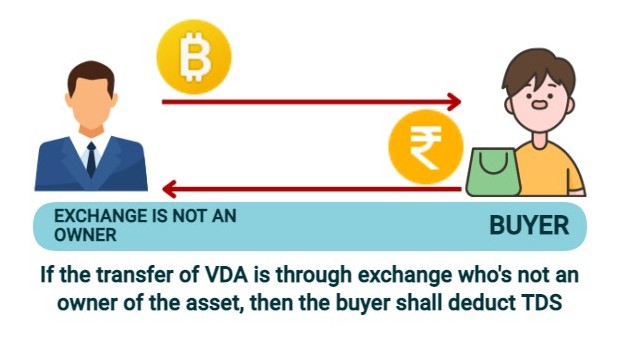

VDA Transfer Through Exchange Who Is Not An Owner Of The Asset

If the transfer of VDA is through exchange who is not an owner of the asset, then the buyer shall deduct TDS under Section 194S. However, there may be cases wherein the buyer may not be aware whether the exchange is the owner of the asset or not. Therefore, to remove this confusion, the circular states the exchange may enter into a written agreement with the buyer or his broker. The agreement may state that in regard to all such transactions the exchange would be paying the tax on or before the due date for that quarter.

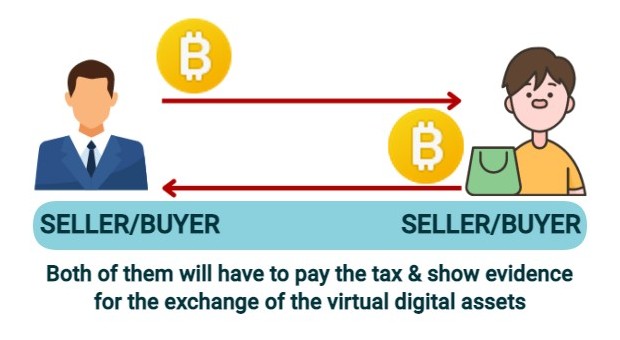

Transfer Of VDA For Another VDA

If the person transfers VDA for another VDA, then both of them will be buyers as well as sellers. Accordingly, in this case, both of them will have to pay the tax and show evidence for the exchange of the virtual digital assets. Further, in this case also the buyer and seller can enter into an agreement for deduction of TDS.

{kind=link}