Share on Social 👇

Updated Income Tax Return – All You Need to Know

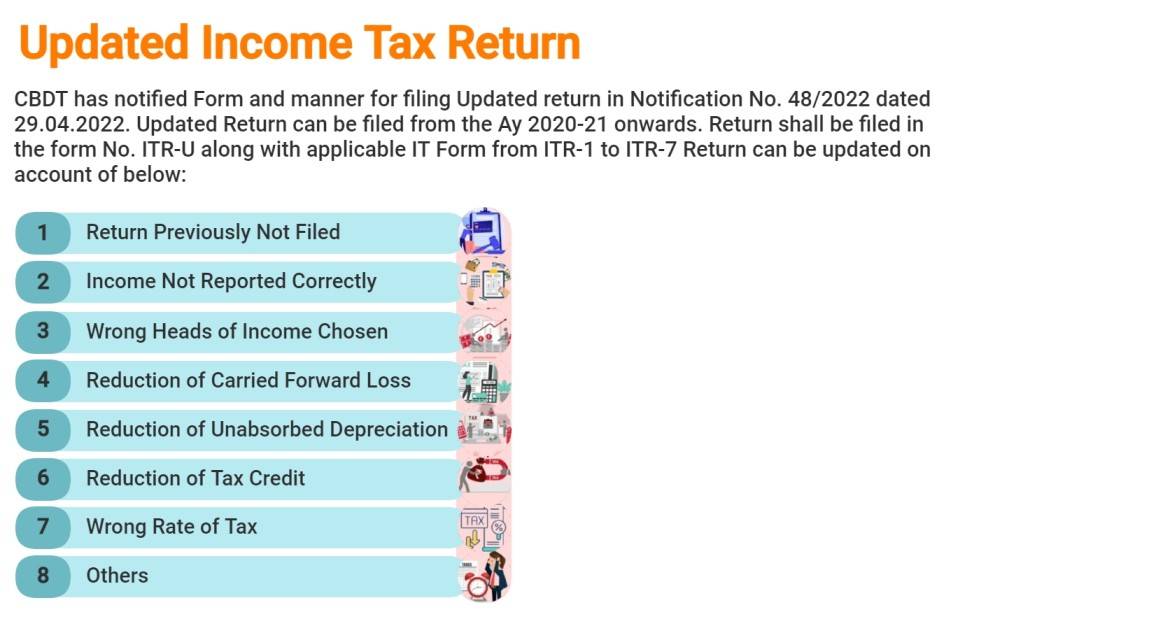

Following are the cases wherein filling of ITR-U is possible:

- Return previously not filed

- Incorrect reporting of income

- Incorrect choosing of the head of income

- Reduction of carried forward loss

- Reduction of unabsorbed depreciation

- Tax credit reduction

- Wrong rate of tax

- Any other case

{kind=link}